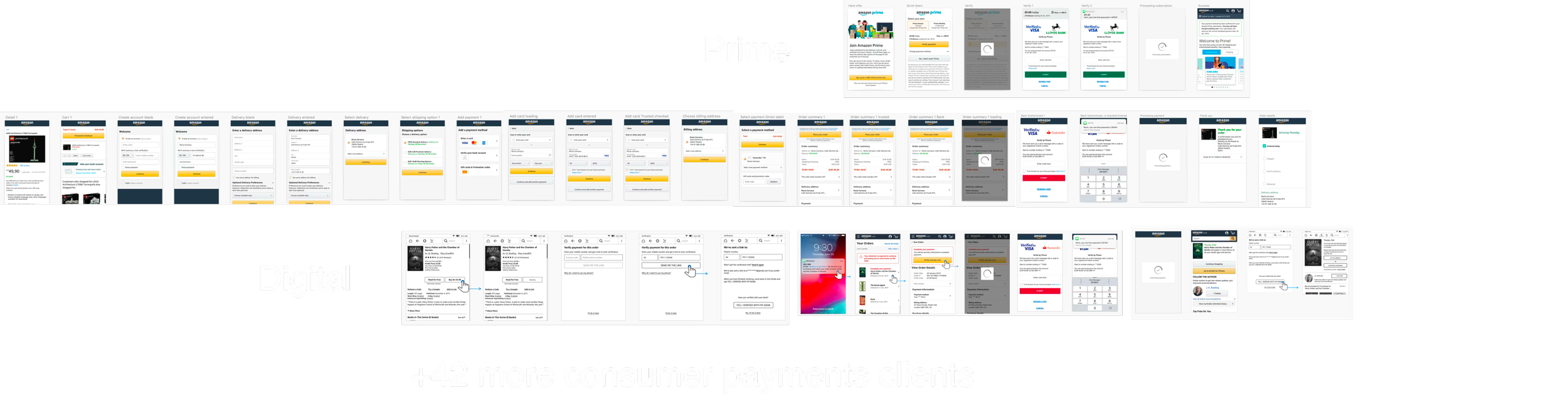

Multi-surface Payments

Amazon EU Payments Re-Architecture

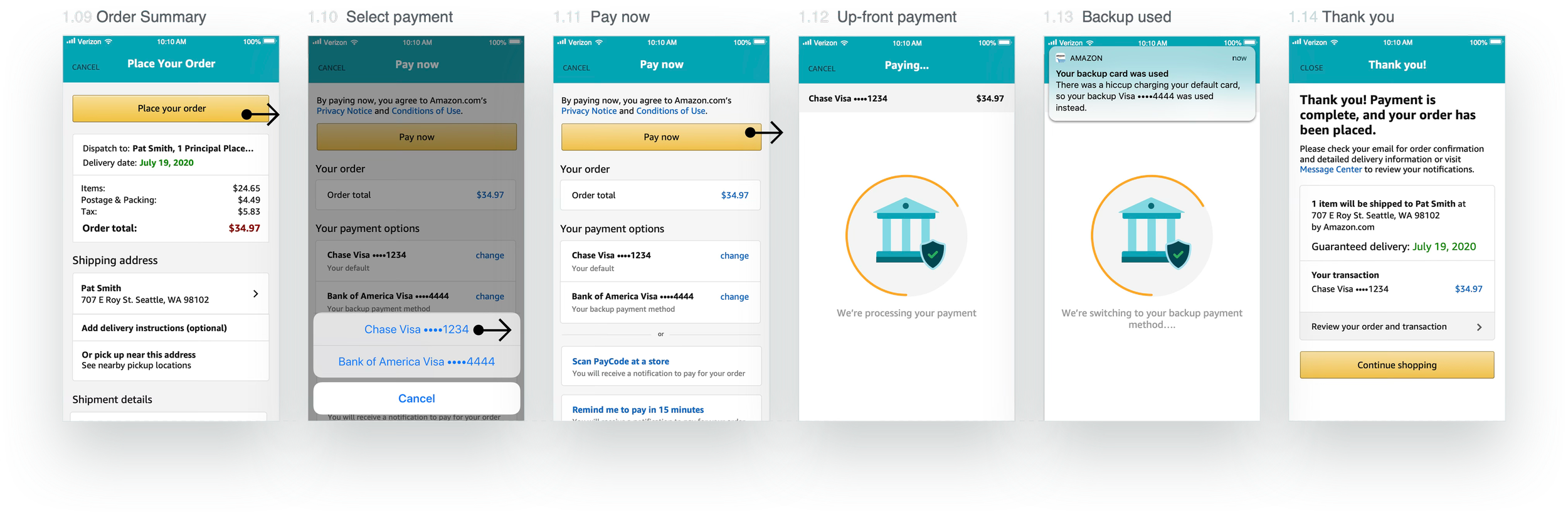

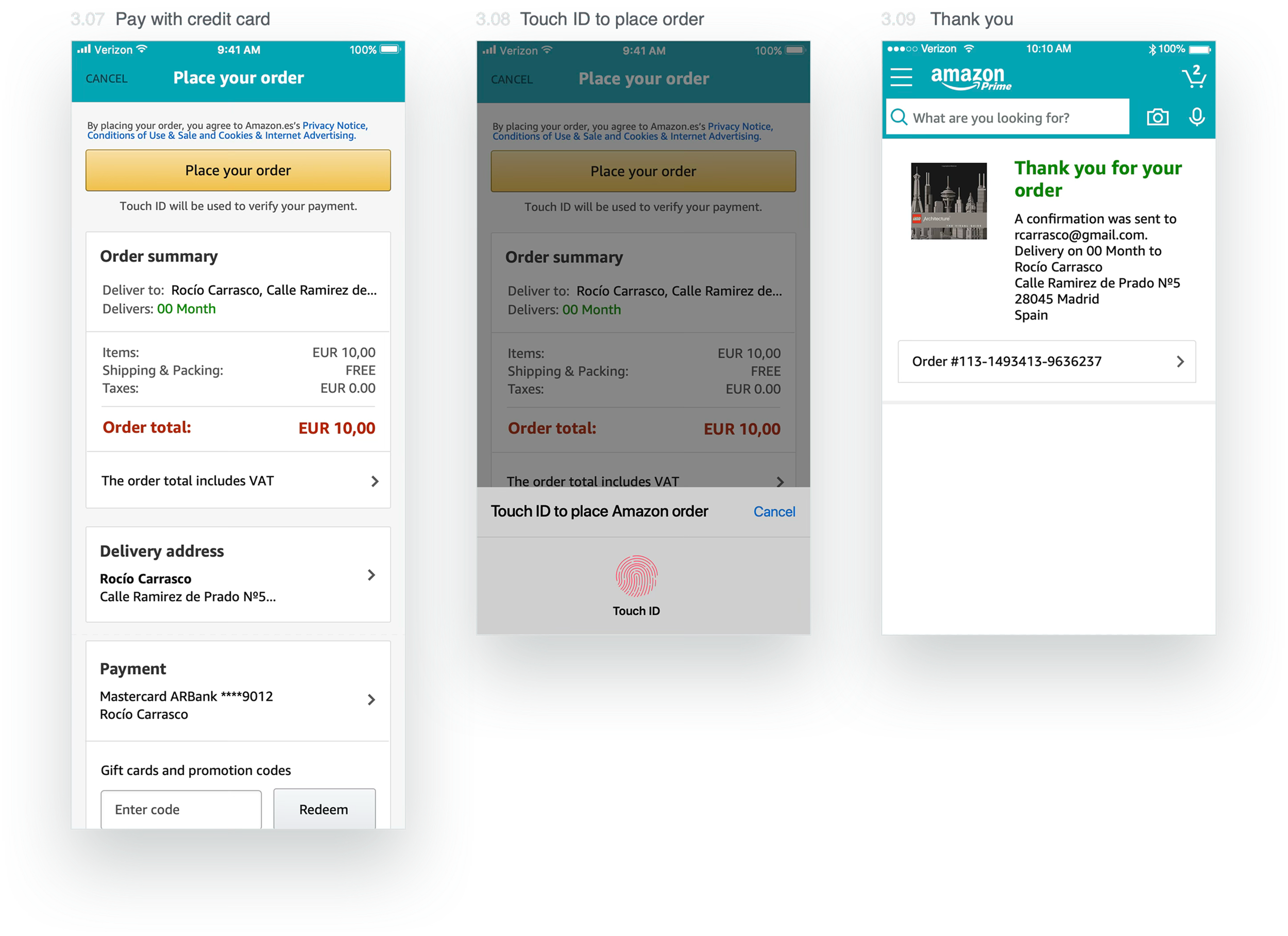

PSD2’s Strong Customer Authentication (SCA) mandate projected $1.9B in 2019 GMS loss across Amazon EU from payment failures, with 3.6MM Prime Members at risk of churning.

I led ethnography and user testing with local users to test Amazon checkout experiences, and created frameworks to align the team on experiences needed to convert first-time, security-conscious new users, and remove friction for high-trust Amazon shoppers purchasing in channels across web, mobile app, voice, and TV.

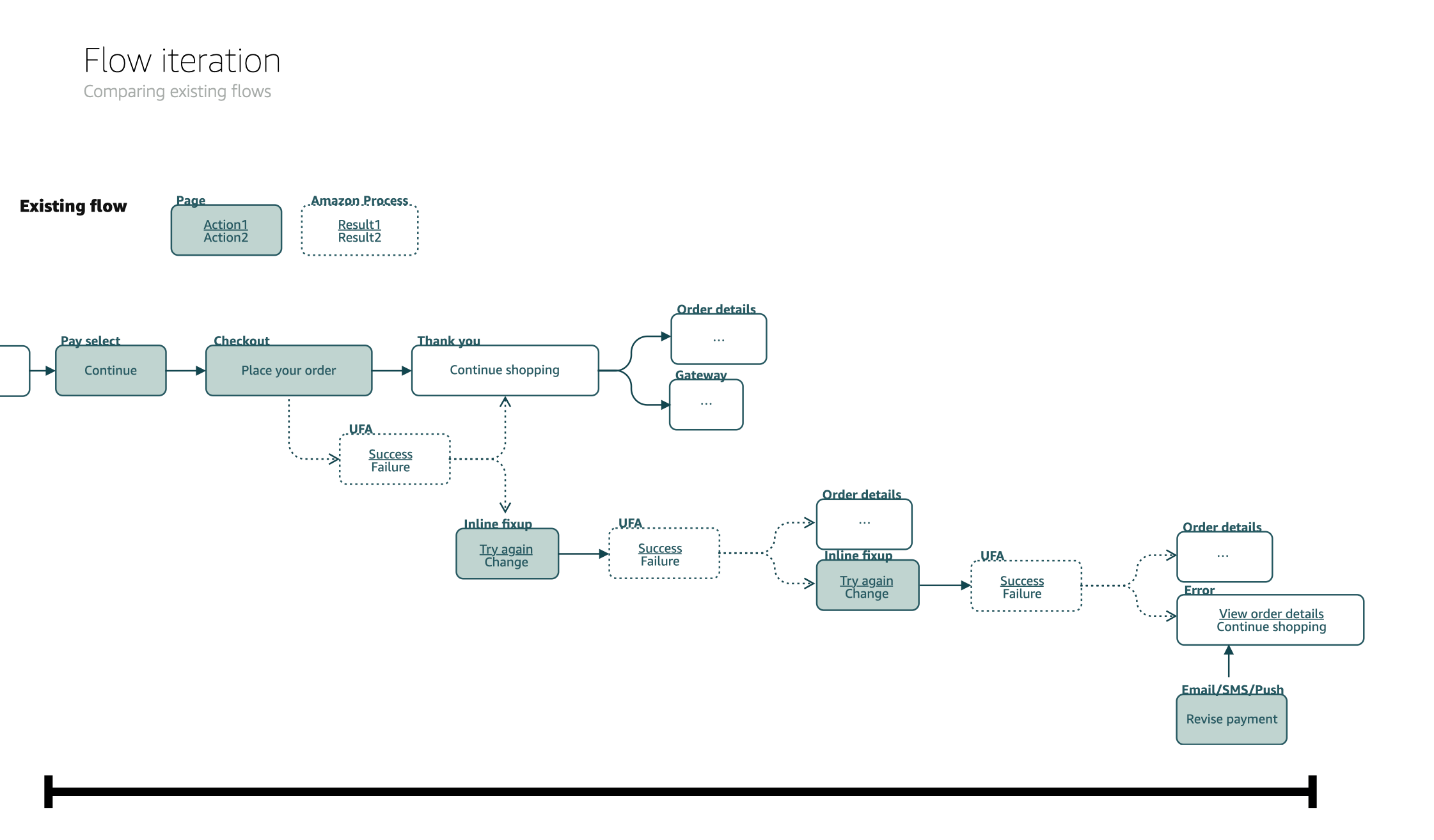

I re-architected EU payments to comply with SCA while preserving conversion across EU 5 (UK, DE, FR, IT, ES) and new locales like CH, and TR.

I prevented ~$241MM in EU GMS loss (25% reduction vs. baseline projection) and retained an estimated 700K+ Prime members. New Pay-at-the-end architecture foundation enabled continued games as SCA expanded into 2020.

Payments widgets embedded in primary retail and subscription workflows.

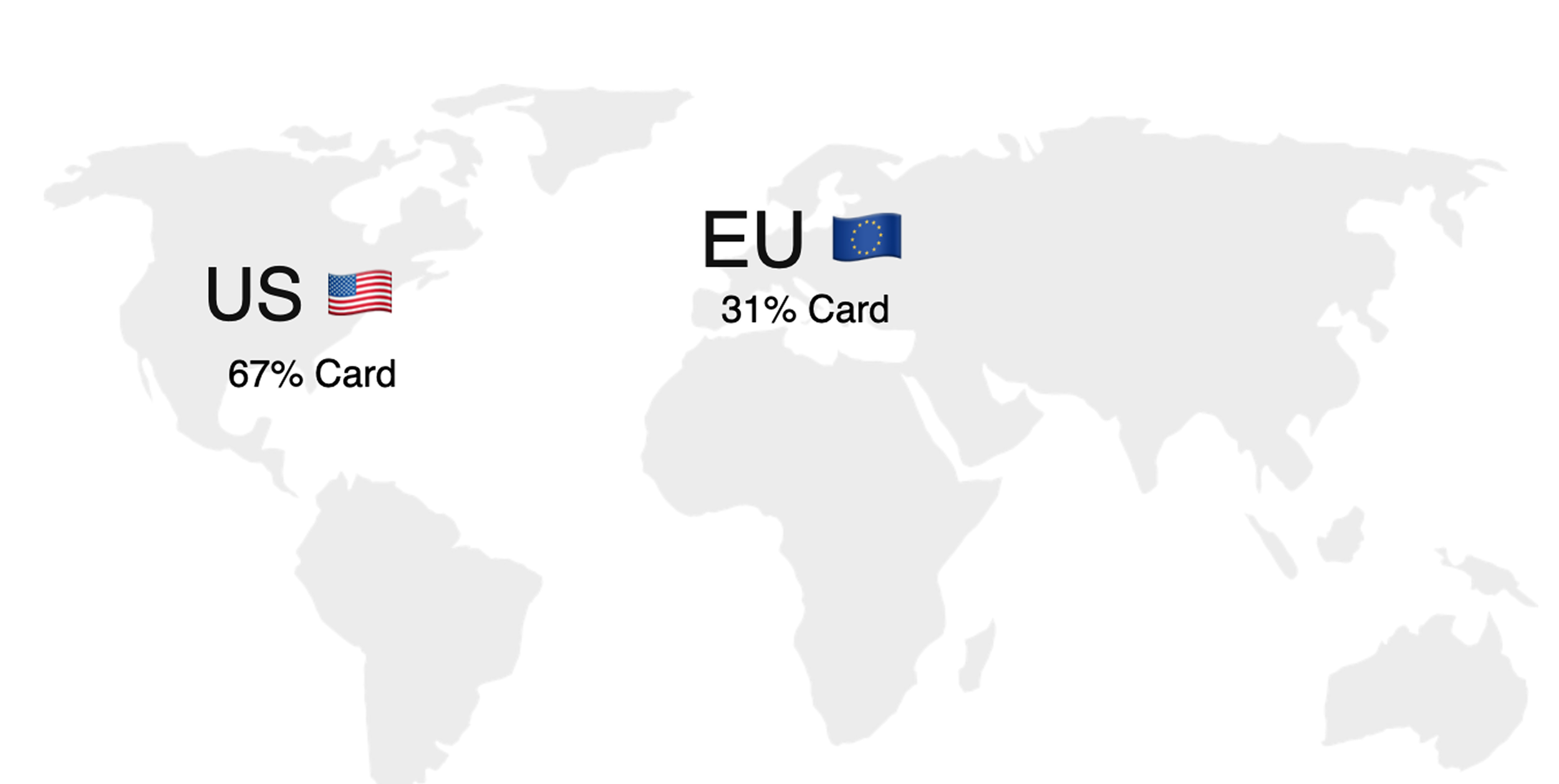

67% vs. 31% card usage in US vs. EU

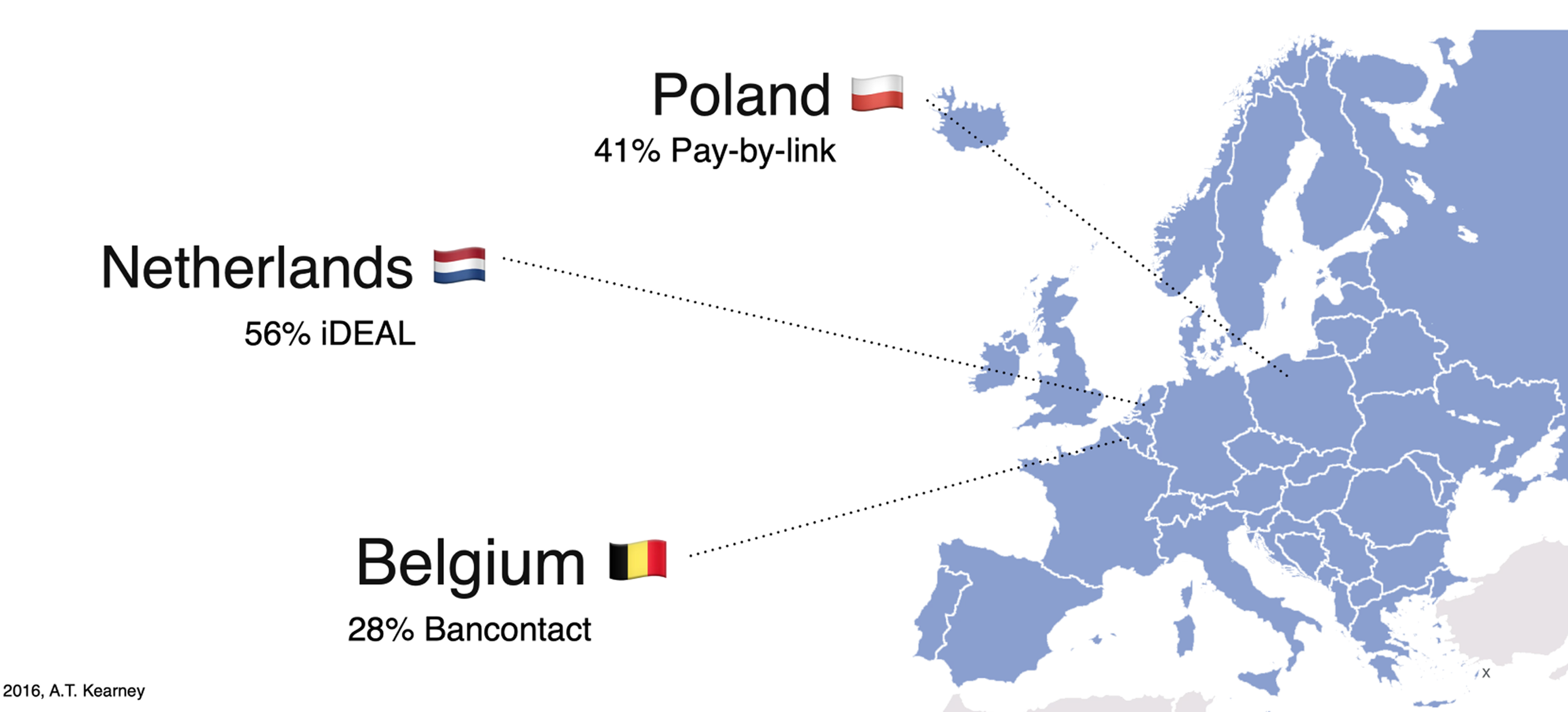

Pay-by-transfer EU customers

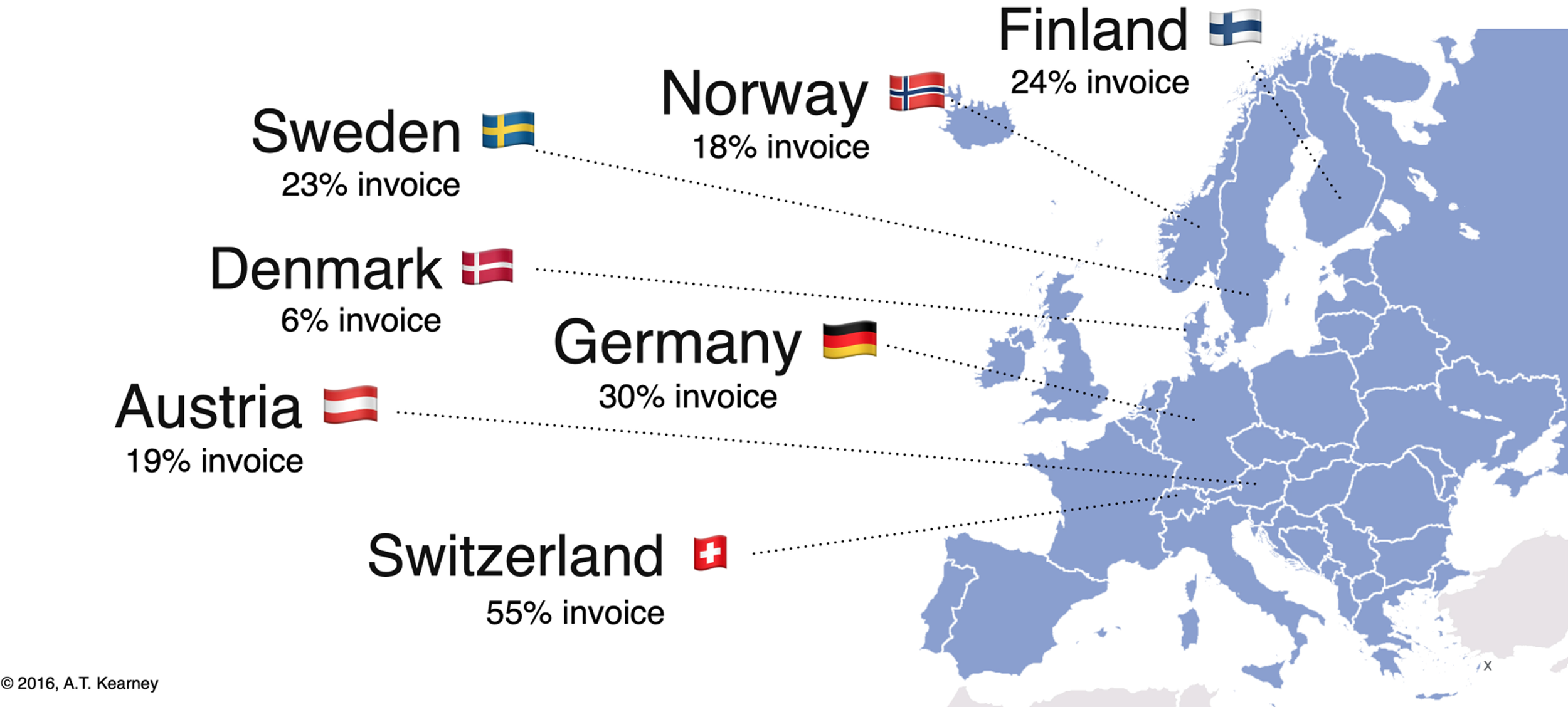

Pay-by-invoice EU customers

Pay-by-transfer and Card authentication

I created a high level journey to synthesize and prioritize the most urgent customer frustrations to improve for the first version of payment by transfer experience for Amazon Retail. This journey also defined the must-haves for this feature to earn the trust of new customers, as Amazon is a new retailer in their countries.

I tested across customer types to accommodate the wide variety of bank and verification styles

Pure app interactions

Dual-device payment verification

Personal Card and Token generator

I iterated and tested a new-to-Amazon polling page, animation and interval for Pay-by-transfer customer to comfortably complete payment on their device while initiating purchases on desktop.

Since the chance for payment failure is increased (compared to credit cards) it was also important to give customers paths to the most successful payment-by-transfer experience, which was mobile. Thus, the final and primary experience was mobile-first, and all error scenarios asked customers to complete payment on the most secure platform, their phone.

These experiences were tested across major Polish, Dutch, and Belgium banks to ensure a high bar across banks that had varied mobile experiences.

Focusing on Pay-by-transfer methods and knowing the similar patterns of experience from credit card authentication, I tested whether the Pay-at-the-end re-architecture could be viable to address payment failures across all redirection-style payment experiences.

Upon launch in 2016, this project challenged the North American shopping and payment journey, and exposed assumptions that didn’t internationalize well to other markets. Given the increased exposure to payment failures and how successful payments are integral to fast delivery to customers, it was crucial to solve this problem for any and all forms of payment failures. With payment-by-transfer, I designed a more general pay-at-the end experience that ensured focus, and inline payment recovery to ensure transparency to the customer and a more guaranteed status of payment and order upon completion.

Pay-by-invoice

To accommodate more types of EU customers, I studied pay-by-invoice customers, I took inventory of the needed artifacts for a successful pay-by-invoice experience on Amazon.

The paper experience was expected for existing invoice customers, but not without frustrations. Losing a paper invoice was costly to customers, and paper invoices tend to get disorganized as customers increase purchases across different retailers with different monthly due dates.

Invoice slip and Bank scanning experience

German invoice variations

Swiss manual post-office invoice payment methods

I designed a digital-first, monthly consolidated Invoice for all purchases digital or physical across of Amazon. There were examples of this already in the industry, both inside and outside Amazon, so I made sure to leverage on strengths of existing solutions while emphasizing the major information needed for smaller screens.

Existing German (by request only) Physical Invoice

Pay after concept

Local competitors consolidating invoices across local online retailers (Klarna)

The design of the monthly invoice page includes states of not paid, and paid, with corresponding schedules of in-app notifications alerting them of major events like invoice close, 3 days before invoice due (the amount of time for the slowest payment method - bank transfer - to complete without fees), and the delightful conclusion: paid.

The final design of the monthly invoice page needed to be a consolidated page that gave customers confidence of what was purchased, the running total, when it was due, and how to pay.

Desktop customers can also replicate a paper-like experience if they print their invoices from the website.

Customers appreciated the clear division of products bought in a month and payment information, which felt to them as flexible and comfortable as the payment method itself. Other invoices lead with the payment information, which customers found pushy.

Amazon Verify

To continue momentum of payment experience expansion and scaling, I explored how one-time, subscription, and authentication payment experiences would look like on Alexa voice, focusing on frictionless ordering and payments, and the smoothest possible experience when an unauthorized user placed an order on an Amazon Alexa device.

Winner of 2018 Payments Hackathon

This was a collaboration with the Alexa Organization, and helped communicate the use case of Alexa needing to verify unique customers from their voice.

Cash payments

Continuing momentum to provide Amazon payments access to all users, I pursued aimed to increase access of Amazon Retail to 51M underbanked and 16M unbanked population. Amazon had silently marginalized customers who don’t want or didn’t have the ability to pay with credit cards or debit cards, and I designed the interface in the project’s effort to unlock Amazon for these customers.

Here, a customer who didn’t want to use cards can instead store a cash balance in their Amazon account to use for purchases. This balance can be reloaded at an increasing number of physical locations, but found with user research that 80% of the time, the customer will be using one familiar location, so it was important to be able to export the barcode for easy access outside of the shopping app.